Optimizing US Tax Deductions: 7 Lesser-Known Opportunities for 2026

In 2026, optimizing U.S. tax deductions requires moving beyond standard write-offs to embrace sophisticated, lesser-known opportunities.

As tax regulations evolve, early awareness of these specialized deductions—ranging from “green” home energy credits to remote-work equipment—can yield significant savings.

This guide provides a factual overview of seven overlooked strategies designed to help taxpayers minimize liability and enhance their 2026 financial planning.

Navigating the Evolving Tax Landscape for 2026

The U.S. tax system undergoes continuous adjustments, making it essential for taxpayers to stay current with the latest provisions.

For 2026, several subtle shifts and existing but underutilized rules present unique opportunities for strategic financial planning.

These changes, often overlooked in the broader discussion of tax reform, can significantly impact an individual’s or business’s bottom line. Proactive engagement with these details is critical for maximizing deductions and ensuring compliance.

Our analysis provides a focused look at areas where astute taxpayers can find advantages. We aim to demystify complex regulations and highlight practical applications for these specific opportunities.

Understanding the Tax Cuts and Jobs Act (TCJA) Sunset Provisions

Many provisions of the Tax Cuts and Jobs Act (TCJA) of 2017 are scheduled to expire at the end of 2025, impacting the 2026 tax year.

This sunsetting will revert several key tax rules to their pre-TCJA status, creating both challenges and opportunities for taxpayers.

Understanding which provisions will expire and how that will affect itemized deductions, personal exemptions, and certain business write-offs is crucial.

This knowledge allows for advanced planning to mitigate potential increases in tax liability or leverage new deductions.

For instance, the increased standard deduction is set to revert, potentially making itemizing deductions more favorable for many taxpayers once again.

This shift underscores the importance of meticulously tracking all eligible expenses.

The Importance of Proactive Tax Planning

Effective tax planning is not merely a year-end activity but an ongoing process that requires foresight and continuous adjustment. For 2026, given the anticipated changes, this proactive approach is more critical than ever.

Engaging with a qualified tax professional early in the year can help identify personalized strategies tailored to individual financial situations. This ensures that taxpayers are not only compliant but also fully optimized in their deduction claims.

Regular reviews of income, expenses, and investment portfolios allow for timely adjustments to capitalize on emerging opportunities. This continuous monitoring is a cornerstone of successful tax optimization.

Exploring Lesser-Known Medical Expense Deductions

While many taxpayers are aware of the general medical expense deduction, several specific categories often go unclaimed.

These deductions, if properly documented, can significantly reduce taxable income, particularly for those with chronic health conditions or unique medical needs.

The threshold for deducting medical expenses remains a key factor, but understanding what qualifies beyond standard doctor visits is essential. This section unpacks some of these less obvious but equally valid deductions.

By meticulously tracking all health-related outlays, taxpayers can uncover substantial savings. This requires a shift in perspective from traditional medical billing to a broader view of health-related expenditures.

Long-Term Care Insurance Premiums

Premiums paid for qualified long-term care insurance policies can be deductible, subject to age-based limits set by the IRS. This deduction is often overlooked, despite the increasing cost of long-term care services.

The deductible amount varies based on the taxpayer’s age, with higher limits for older individuals. This incentive encourages planning for future healthcare needs while offering immediate tax relief.

It is important to ensure the policy meets IRS qualification standards to claim this deduction. Consulting with an insurance or tax professional can clarify eligibility and maximum deductible amounts.

Home Improvements for Medical Care

Modifications made to a home for medical care purposes can be fully or partially deductible. This includes expenses for installing ramps, widening doorways, or even modifying bathrooms to accommodate a disability.

The key is that these improvements must primarily be for medical care and not for general home improvement or aesthetic value. Any increase in the home’s value due to the improvement must be subtracted from the deductible amount.

Maximizing Education-Related Tax Benefits

Beyond the more commonly known student loan interest deduction and education credits, there are specific scenarios where educational expenses can lead to significant tax savings.

These often involve specialized training or professional development directly related to employment.

Understanding the distinction between education that maintains or improves job skills versus education that qualifies for a new career is crucial. The former is generally deductible, while the latter is not.

For those pursuing continuing education or professional certifications, these deductions can be a powerful tool for reducing tax burdens. Proper documentation of course relevance and expenses is key.

Work-Related Education Expenses

Expenses for education that maintains or improves skills required in your current job can be deductible as an itemized deduction. This includes tuition, fees, books, supplies, and even transportation costs for attending classes.

The education must not be required to meet the minimum educational requirements of your current job, nor can it qualify you for a new trade or business. These nuances are critical for successful claims.

Examples include a lawyer taking a tax law course, or a teacher attending a seminar on new teaching methods. Such expenses directly enhance current professional capabilities.

Educator Expenses for K-12 Professionals

Eligible educators can deduct up to a certain amount for unreimbursed ordinary and necessary expenses paid for books, supplies, computer equipment (including related services and software), other equipment, and supplementary materials used in the classroom.

This deduction is available even if you don’t itemize, making it particularly valuable for K-12 teachers, instructors, counselors, principals, or aides who work at least 900 hours during the school year.

The deduction helps offset the personal financial contribution many educators make to their classrooms. Keeping detailed records of purchases is essential for claiming this benefit.

Unlocking Home Office and Business Deductions

The rise of remote work has made the home office deduction more relevant than ever, yet many eligible individuals fail to claim it due to perceived complexity or unawareness of its full scope.

Beyond the basic deduction, there are intricacies that can further optimize this benefit.

For self-employed individuals and certain employees, a dedicated home workspace can unlock a range of deductions. These extend beyond rent or mortgage interest to include utilities, insurance, and repairs.

Properly distinguishing between personal and business use of a home is paramount for compliance and maximizing claims. The IRS has strict guidelines that must be adhered to.

Simplified Home Office Deduction

For those who qualify for the home office deduction, the IRS offers a simplified option that allows a standard deduction per square foot of home office space, up to a maximum area. This streamlines the process significantly.

While the simplified option may not yield as large a deduction as the actual expense method for some, it reduces the record-keeping burden. It provides a straightforward way to claim a legitimate business expense without extensive calculations.

Taxpayers should compare both methods to determine which offers the greater benefit based on their specific situation. This comparison is a key aspect of Optimizing Your US Tax Deductions: 7 Lesser-Known Opportunities for 2026.

Business Use of Your Car

If you use your personal vehicle for business purposes, you can deduct the actual expenses or use the standard mileage rate. This includes travel to client meetings, business conferences, or transporting goods.

Keeping a detailed mileage log is crucial, regardless of the method chosen. This log should record dates, destinations, business purposes, and miles driven for each trip.

For the actual expense method, you can deduct costs like gas, oil, repairs, insurance, and depreciation. The choice between methods depends on individual driving habits and vehicle costs.

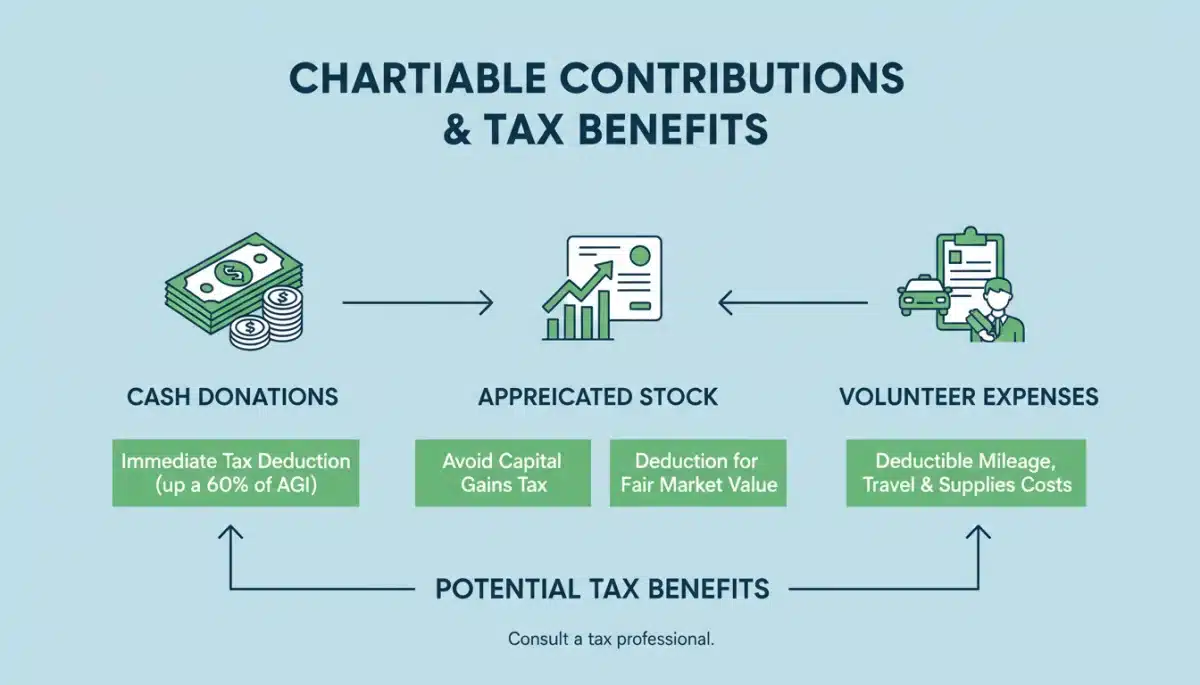

Leveraging Charitable Contributions Strategically

Charitable giving is not only a philanthropic act but also a powerful tool for tax planning. Beyond simple cash donations, various forms of contributions can offer unique tax advantages, especially when structured thoughtfully.

Understanding the rules for donating appreciated assets, volunteer expenses, and even certain out-of-pocket costs for charitable activities can significantly enhance your deduction.

These methods often provide greater tax benefits than direct cash gifts.

Strategic charitable giving, especially for high-net-worth individuals, forms a critical component of Optimizing Your US Tax Deductions: 7 Lesser-Known Opportunities for 2026. It requires careful planning and documentation.

Non-Cash Charitable Contributions

Donating appreciated stock or other non-cash assets held for more than a year can be more tax-efficient than donating cash. You can typically deduct the fair market value of the asset and avoid capital gains tax on the appreciation.

This strategy allows you to support your chosen charities while also reducing your personal tax burden. The IRS has specific rules for valuing non-cash contributions, especially for items above a certain value.

Items like clothing, household goods, or even vehicles can also be deductible. It is essential to obtain a written acknowledgment from the charity for any contribution over a certain amount.

Volunteer Expenses

While you cannot deduct the value of your time spent volunteering, out-of-pocket expenses incurred while performing services for a qualified charity are deductible.

This includes mileage driven for charitable purposes, parking fees, and the cost of uniforms or supplies.

These expenses must be un-reimbursed and directly related to the charitable work. Keeping meticulous records, such as mileage logs and receipts for purchases, is vital.

This deduction often goes unclaimed, as many volunteers are unaware that these costs are eligible. It represents a significant opportunity for those dedicated to charitable causes.

Exploring Investment-Related Deductions

Beyond the standard capital gains and losses, there are several less common investment-related deductions that can help reduce your overall tax burden. These often relate to specific types of investments or expenses incurred in managing them.

Understanding these intricacies is crucial for investors seeking to optimize their portfolios from a tax perspective. They can provide avenues for savings that are not immediately apparent.

For 2026, with potential shifts in market conditions, these deductions could become even more valuable. Diligent record-keeping of all investment activities remains a cornerstone of successful claims.

Investment Interest Expense

You can deduct investment interest expense up to the amount of your net investment income. This includes interest paid on money borrowed to purchase taxable investments, such as margin interest.

This deduction is an itemized deduction, meaning it’s only beneficial if your total itemized deductions exceed the standard deduction. It’s an important consideration for active investors utilizing leverage.

Careful tracking of both investment interest paid and investment income received is necessary to correctly calculate and claim this deduction. This can be a key part of Optimizing Your US Tax Deductions: 7 Lesser-Known Opportunities for 2026.

Casualty and Theft Losses on Investment Property

While personal casualty and theft losses are largely disallowed under current tax law, losses on investment property can still be deductible. This applies to events like natural disasters or theft that impact assets held for investment.

The loss must be sudden, unexpected, or unusual. The deductible amount is generally the lesser of the adjusted basis of the property or the decrease in its fair market value, reduced by any insurance reimbursements.

Documenting the loss, including police reports, insurance claims, and appraisals, is essential for substantiating this deduction. This can provide relief in unfortunate circumstances.

Deductions for Job Search and Moving Expenses

Certain expenses incurred during a job search or for moving due to a new job can be deductible, though the rules have become more restrictive in recent years. Understanding these specific conditions is crucial for eligible individuals.

For the 2026 tax year, it’s important to differentiate between general job search activities and those that meet the IRS’s strict criteria. Similarly, moving expenses have limited applicability.

These deductions, while not universally available, can offer significant relief to those who qualify. They are often overlooked due to their specific requirements.

Job Search Expenses (for Self-Employed or Certain Professions)

While most employees can no longer deduct job search expenses, self-employed individuals looking for a new business, or individuals seeking employment in the same line of work, may still qualify. This includes expenses for résumés, travel, and employment agency fees.

The key is that the job search must be in your current line of work. If you are looking for a job in a new occupation, these expenses are generally not deductible.

Keeping detailed records of all job search-related expenses is essential for supporting any claims. This can be a valuable, though specialized, deduction.

Moving Expenses for Armed Forces Members

For 2026, the deduction for moving expenses is generally suspended for most taxpayers. However, an exception exists for members of the Armed Forces on active duty who move due to a permanent change of station.

This specific deduction covers reasonable unreimbursed expenses for moving household goods and personal effects, and for traveling to the new home. It’s an important benefit for military families.

Understanding the specific criteria for a permanent change of station and maintaining thorough records of all moving-related costs is vital for claiming this exception.

Miscellaneous Itemized Deductions (Limited Scope)

While the TCJA suspended most miscellaneous itemized deductions subject to the 2% adjusted gross income (AGI) floor, a few specific categories remain deductible. These are highly specialized and often apply to unique situations.

It’s crucial to be aware of these remaining deductions, as they can still provide valuable tax relief for those who meet the strict criteria. Many taxpayers mistakenly believe all such deductions are gone.

For 2026, verifying which specific deductions are still active and applicable to your situation is a key step in Optimizing Your US Tax Deductions: 7 Lesser-Known Opportunities for 2026. This requires careful review of current tax law.

Gambling Losses Up to Winnings

You can deduct gambling losses up to the amount of your gambling winnings as an itemized deduction. This deduction is not subject to the 2% AGI floor, making it one of the few remaining miscellaneous itemized deductions.

It’s important to keep accurate records of both winnings and losses, including dates, amounts, and locations. You cannot deduct more in losses than you report in winnings.

This deduction applies to all forms of gambling, from lotteries to casino games, as long as you can substantiate both the winnings and the losses. This is a targeted deduction for a specific activity.

Certain Impairment-Related Work Expenses

Employees with disabilities can deduct certain impairment-related work expenses as a miscellaneous itemized deduction not subject to the 2% AGI limit. These expenses must be necessary for them to work.

Examples include the cost of a wheelchair, a personal assistant to help with work duties, or specialized equipment. These expenses must be directly related to enabling the individual to perform their job.

This deduction provides crucial support for individuals with disabilities to participate in the workforce. Detailed documentation of the expenses and their necessity is required.

| Key Opportunity | Brief Description |

|---|---|

| Long-Term Care Premiums | Deductible based on age, supporting future healthcare costs. |

| Work-Related Education | Expenses for maintaining or improving current job skills. |

| Non-Cash Charitable Gifts | Donating appreciated assets for greater tax efficiency. |

| Simplified Home Office | Streamlined deduction for qualified home office use. |

Frequently Asked Questions About 2026 Tax Deductions

The most significant changes for US Tax Deductions 2026 stem from the sunsetting of many TCJA provisions. This means a potential reversion to pre-2018 tax laws, affecting itemized deductions, personal exemptions, and certain business write-offs. Staying informed about these expirations is crucial for effective planning.

To identify lesser-known but deductible medical expenses, consider costs beyond standard doctor visits. Examples include long-term care insurance premiums (age-limited), home improvements for medical care, and certain addiction treatment programs. Always keep detailed records and consult IRS Publication 502 for comprehensive guidance on what qualifies.

For most employees, work-related education expenses are generally no longer deductible as miscellaneous itemized deductions. However, self-employed individuals may still deduct education that maintains or improves skills for their current trade or business. Educators, specifically K-12, retain a limited above-the-line deduction for classroom expenses.

Donating appreciated stock held for over a year offers dual benefits: you can deduct the fair market value of the stock and avoid paying capital gains tax on its appreciation. This typically results in a larger tax deduction and greater overall savings compared to donating an equivalent amount in cash, maximizing your charitable impact.

The home office deduction for employees was suspended by the TCJA and is not expected to return for 2026. This deduction is primarily for self-employed individuals who use a portion of their home exclusively and regularly for business. Employees working remotely generally cannot claim this deduction.

Conclusion

As the financial landscape becomes more complex, the value of a proactive, top-down investment approach becomes even more apparent.

By analyzing global economic, political, and sentiment factors first, investors can identify opportunities across categories before narrowing down to specific securities.

Managing wealth in 2026 is no longer just about picking stocks; it is about building a resilient ecosystem that adapts to both market shifts and individual life milestones.

To explore how personalized strategies can secure your financial future, you can visit the latest wealth management and investment planning insights from Fisher Investments.